Charity is Theft: The Gann Foundation and Boston’s Zionist NGO circuit

Non-profits and charities are theft. Charitable foundations are onshore tax havens, and charitable “gifts” are tax evasion scams. Even starting from this place of truth, the massive amount of wealth hoarding conducted by and for rich people is staggering. As members of the Mapping Project collective, we have contributed to articles about 37 non-profits, charities, and non-governmental organizations, and none of them have lessened the truth: charitable giving is a way for rich people to amass money—power—and then grant it as they see fit personally, enriching their allies, and bypassing much-needed resource redistribution. The concentration of wealth in New England demonstrates the importance of combatting zionism locally. In 2019, Massachusetts had the third highest median income in the united states. The twelfth largest bank (by amount of capital held) in the united states, State Street, is headquartered in Boston, MA and holds over $318 million assets across only 12 bank branches in the world. With tremendous money available for wealth hoarding, New England is ripe for tax evasion through charitable entities. We can directly tie the non-profit industrial complex to the colonization of Palestine, demonstrating that the united states tax code facilitates the laundering of wealth from the richest people in the united states to organizations supporting zionism and the genocide in Palestine (beyond the regular dispersal of united states tax dollars in support of the occupying power).

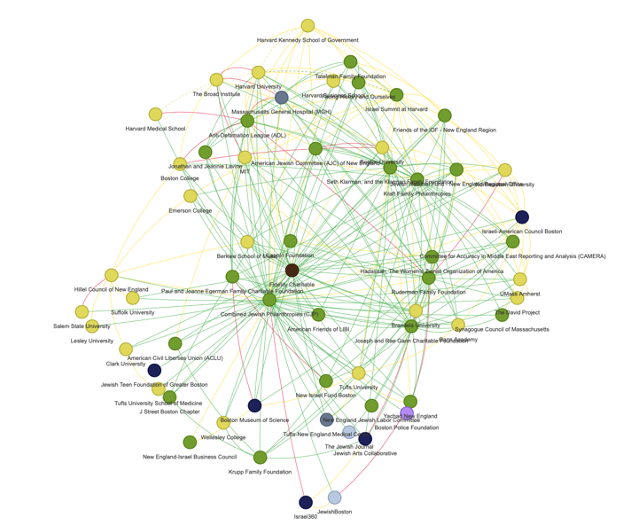

The Mapping Project contains a non-exhaustive list of numerous non-profits/non-governmental organizations (NGOs) operating in Massachusetts that contribute to the genocide against Palestinians in their homeland and the criminalization of Palestinian identity in diaspora. The very existence of these organizations, sheltered from taxes and operating often expressly to further the colonization of Palestine, betrays that charities simply do not operate for public good.

These organizations vary in size and stated purpose. Most are public charities, which will be defined in a different section of this essay. About sixteen of these organizations have missions explicitly tied to normalizing zionism and material support for the state of israel. Many of these organizations are the New England or Massachusetts regional office of a national NGO (like Friends of the IDF – New England or the New Israel Fund Boston). Considering that Jewish National Fund (JNF) National organization received ~$85 million dollars in 2020 in donations, and that in 2021, the New England branch was able to raise ~11.4 million dollars alone, the map has only confirmed the staggering impact of regional offices on the national zionist project. Because these entities also work on behalf of “israeli pride” and even for the direct colonial expansion of the state, such as the JNF, they are the very clear examples of political entities masquerading as organizations apolitically supporting all peoples. Additional distinctions can be made between the rest of the organizations. Four are NGOs offering services to fill gaps in the social safety net with a zionist ideology guiding their work. Another four are NGOs reinforcing business ties between the united states and israel.

Nine NGO entities are private foundations (or similar), which are the focus of this essay. They include:

|

Name |

Value as of most recent form 990 |

Zionist institution receiving the most donations historically |

Total wealth funneled to zionist organizations |

|

~$2.7 Million (2019) |

Combined Jewish Philanthropies (CJP) |

~$1.4 Million (FY 2004-2019) |

|

|

~$839 Million (2019) |

Combined Jewish Philanthropies (CJP) |

~$85.2 Million (FY 2004-2019) |

|

|

~$24.4 Million (2019) |

Combined Jewish Philanthropies (CJP) |

~$2.1 Million (FY 2001-2019) |

|

|

~$184 Million (2019) |

Combined Jewish Philanthropies (CJP) |

~$36 Million (FY 2001-2019) |

|

|

~1.3 Million (2019) |

n/a |

~$479,000 (FY 2016-2018) |

|

|

~$45.5 Million (2020) |

Combined Jewish Philanthropies (CJP) |

$16.5 Million + (FY 2001-2018) |

|

|

~$38.5 Million (FY 2020) |

Gann Academy |

~$5.6 Million (FY 2001-2020)

|

|

|

~$1.6 Billion (FY 2020) |

Jewish Community Relations Council (JCRC) of Greater Boston |

~$137 Million (FY 2007-2020) |

|

|

~$35.3 Billion (FY 2019) |

Friends of the Israeli Defense Forces |

~$69.3 Million (FY 2019-2020) |

For more information on the entities in this chart, please visit the Mapping Project – NGO entity list. Several entities include partial information on donation totals. Please search ProPublica Nonprofit Explorer to review tax filings of interest.

An Introduction to Non-profits

Representing 79% of all non-profits, the 501c3 tax designation makes an organization tax-exempt. This means the organization owes no income taxes on contributions received, and the individuals who made such contributions can receive a tax deduction on their personal taxes. There are many types of IRS-recognized non-profits, but there is a useful distinction made between public charities and private foundations. Public charities solicit donations from the public, and often offer social services of varying kinds—like the United Way or Habitat for Humanity—not to suggest that they are good organizations, just different from private foundations.

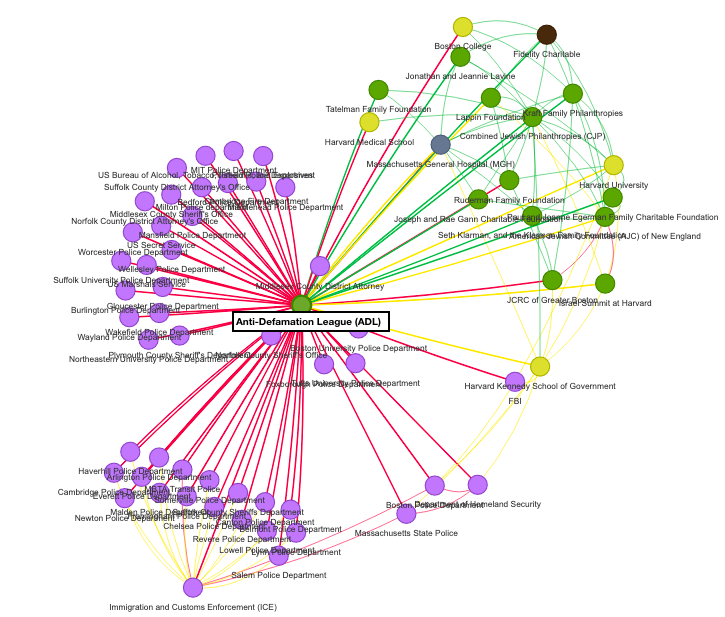

The green entity encircled largely by red lines and lavender dots is the Anti-Defamation League (ADL), and each of the lavender dots is a police department. The red lines symbolize partnership between the entities. The ADL is most notable today (2001-present) for its commitment to connecting militarized and surveillance-focused settlers in occupied Palestine (such as the IDF/IOF) with united states police forces under the guise of “counterterrorism” training. The abuses and historic evolution of police and policing make clear that abolition is the only way forward for humanity, yet the ADL continues to nurture relationships with these agents of state violence. They “encourage united states law enforcement to identify with israel, to view Palestinians as "terrorists," and to view anyone who speaks or acts in solidarity with Palestinians as "terrorist sympathizers… because the ADL is deeply invested in the power and dominance of the united states state itself.”

The ADL is focused on legitimizing the united states colonial project to in turn legitimize the colonial project of “israel,” and helps train the arbiters of state violence to do so. The ADL is directly tied to brutalizing people (most often Black people) through their support of the police in the united states, while propping up the occupiers of Palestine. According to the IRS, this organization is performing a public service—the ADL is an IRS registered tax-exempt public charity. From 2016-2020, the ADL received over $366 million dollars in public donations, essentially tax free. $366 million dollars being funneled into the salaries of the people that connect police internationally, that pay for the travel expenses and meals of the police, that create political messaging suggesting the police serve a necessary function in society; $366 million dollars untaxed being funneled into the pockets of politicians that vote to send more aid to the apartheid regime of israel. The ADL has so much money they started an additional non-profit, the Anti-Defamation League Foundation, through which they monitor some investments. From 2015-2019, the ADL Foundation received over $63 million dollars from the public, and again, use this money to bolster material support for israel.

501c3 organizations are one of the most pervasive and outrageous uses of united states tax code, but this is even more applicable to private foundations. By starting a private foundation, a rich person can take advantage of tax law as an individual (writing-off charitable donations on their income taxes) and as an incorporated body by donating to their own private, tax-exempt foundation. This allows them to reduce their taxable income and avoid taxes completely on 20-30% of their taxable income (described below), all while remaining in control of the “donated” wealth. And this is only one legal tax evasion scheme.

7% of all IRS-recognized non-profits are private foundations, which the Congressional Research Service describes as “tightly controlled, receive[ing] significant portions of their funds from a small number of donors or a single source, and make[ing] grants to other organizations rather than directly carry[ing] out charitable activities." This definition makes clear that private foundations are usually non-operating—they do not perform any direct services or operate any charitable programs. They exist to funnel money to other organizations. The “catch” is that the organizations that private foundations donate to must meet the IRS-definition of a “real” charity. This definition is long, and outlines what “exempt purposes” a charity can operate for, efforts like “preventing cruelty to children or animals” or “relief of the poor, the distressed, or the underprivileged,” but the definition also includes religious organizations (such as churches) and academic institutions (such as private universities). It also states that the act of “lessening the burdens of government” is a legitimate goal—codifying the conservative belief that charity is better than government programs.

The current tax law allows for private foundation non-profits, which supposedly carry-out these activities indirectly through their shifting of funds to public charities. The IRS definition also excludes overtly political activities, like those conducted within the system of electoral politics and lobbying—but we know this rule to be inconsequential. Money is always political, perhaps especially in charitable work, which too often determines everything from the allocation of life-saving resources to the quality of a child’s education.

The Mapping Project has identified numerous examples of the “non-political” fallacy of the 501c3 charity. The American Friends of LIBI is a straightforward example of a “charity” existing for expressly political purposes. LIBI (the Hebrew word for “my heart”) was established in 1980 by Israeli politicians and military figures in israel to support israeli soldiers, and the American Friends of LIBI was established to support the same political purpose in 2004. The summary provided by the American Friends of LIBI on their 2018 tax form expressly states that they “provide…social services to new immigrants and underprivileged persons (and their families)…as they fulfill their commitment to the Israeli Defense Force…” Essentially, by supporting new and impoverished settlers while these settlers violently repress Palestinians in the israeli Occupation Force, American Friends of LIBI is creating another economic incentive to occupy Palestine, helping to dilute what this “service” may cost a settler or their family. The charity believes in the zionist project of israel, an inherently political statement. By this description, it becomes obvious just how many “charities” are political projects in (poor) disguise.

“Everybody” pays taxes: the itemized deduction

The united states government passed the Individual Income Tax Act of 1944 as a measure to raise revenue for use in WWII. 5% of united states citizens paid federal taxes in 1939, while 75% of united states citizens paid income taxes in 1944. This Tax Act also introduced the standard deduction. Simplified, there are two ways to calculate taxes owed to the federal government—the standard deduction or the itemized deduction. The standard deduction is the amount set by the federal government, adjusted for inflation, that any person may deduct from their income. This reduces the tax bracket of the taxpayer, by lowering the total amount of income they must pay taxes on. Most people pick the standard deduction, as it significantly drops their tax bracket, reducing the percent at which their income is taxed. If an individual makes a lot of money, so much that the standard deduction would not drop their tax bracket in a meaningful way, they choose to itemize deductions. With this process, the taxpayer painstakingly lists all actions they took in the previous tax year to lower their income bracket/reduce their taxable income. This is done through legally permissible deductions and tax credits, created by the federal government to incentivize specific behaviors. Itemized deductions not only exceed the standard deduction in dollar amount but substantially decrease the percentage of the rich taxpayer’s income taxed within the tax year. Because accounting for hundreds of thousands of dollars is a full-time job, these taxpayers employ other people to file their taxes—sometimes teams of accountants and tax lawyers.

The problem with current tax structure is immediately evident—the stance of tax law is to incentivize the richest people in the united states to comply with the law by meaningfully lowering their total percentage of income given in taxes relative to the average united states taxpayer. Unlike most folks, the wealthiest people can choose to subvert the law, while rarely facing consequences. Tax law exists to beg rich people to support the public good rather than requiring this support. Some estimates suggest that, in 2019, just 11% of united states taxpayers itemized deductions. In 2017, 93% of taxpayers with income above $500K elected to use itemized deductions, demonstrating the itemized deduction was made to pacify the rich.

The attraction of the itemized deduction is the ability to claim numerous deductions and tax-credits that cumulate in a taxable income reduction of far more money than the standard deduction. Tax credits disproportionally benefit the wealthy, providing discounts for homeownership and sales of property, dependents (children, not other family in need of care), and, of course, charitable donations.

The itemized deduction at work: “charitable giving”

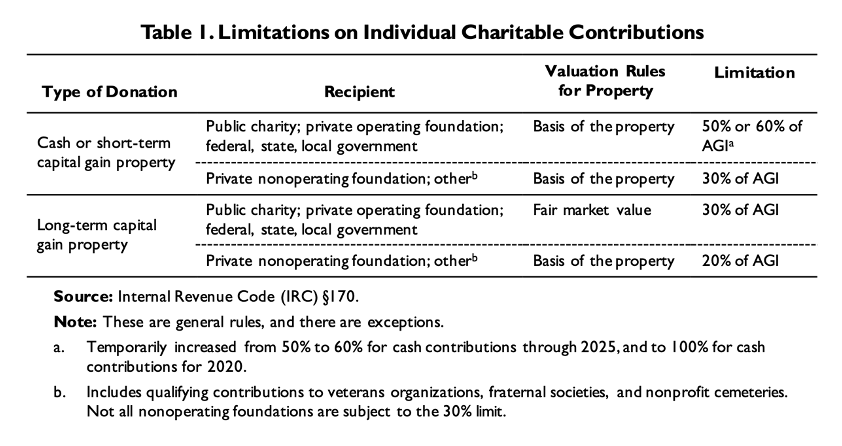

A rich person calculating their taxes through itemized deduction can write-off up to 60% of their income donated to a public charity, provided it is represented by cash or short-term held stocks. If they choose to donate “long-term capital gain property”—stocks and other securities held for over a year—they can write-off up to 30% of their income and will circumvent capital gains taxes on the appreciation of the stock since its purchase. Rich people still dislike this option—why?

By “gifting” money or securities to a public charity, they lose most of their legal control over the funds. Donors gain influence, politically and beyond, that well exceeds the value of any figure they give, but unless the rich are directly involved with the charity, they ultimately cede control of the assets upon donating (with a few caveats). Private non-operating foundations solve this dilemma and allow the wealthy to retain control of their assets legally while dramatically decreasing their tax bill. The cash amounts are reduced, but a rich person can still donate 30% of their income in cash to a private, non-operating foundation, and thereby reduce their income bracket. If they choose to donate stocks, as previously described, they can still write-off up to 20% of their income and any capital gains taxes that may have applied to those long-term securities.

Some additional rules apply to private, non-operating foundations. In order to make private foundations actually disperse assets (i.e. give money to charitable organizations that actually do something/operate programs), they are required to make “contributions, gifts, and grants” annually, a minimum of 5% of the assets of the Foundation. This is called a “payout requirement.” Additionally, securities (like stocks, bonds, financialized imaginary money) seeing capital gains that are owned by the private foundation are subject to a 1.39% tax, as of 2020. Both these rules intend to limit the amount of wealth-hoarding possible, but instead exist as tax benefits for the rich. Putting stocks in a family foundation means that capital gains are taxed at 1.39% rather than at 20%, the rate for the highest tax income bracket. Additionally, the 5% rule is so low that private foundations often just use the undertaxed securities to make donations, allowing the original money transferred into the foundation to remain untouched and the value of the foundation to grow.

To put this into perspective, the federal government allowed those taking the standard deduction to write-off $300 ($600 for married couples) of contributions to 501c3 recognized charities in 2021—considering that the median united states household income was $67,521 in 2020, and accounting for the standard deduction, this allowed for an extra tax deduction of .54%-1.11% based on charitable contributions for the average unites states tax payer. Contrast this with the potential 60% write-off for taxpayers filing with an itemized deduction.

Tax evasion case study: the Joseph and Rae Gann Charitable Foundation

The Mapping Project has demonstrated numerous examples of legal tax evasion. For example, the Joseph and Rae Gann Charitable Foundation's tax filings from the past two decades Fiscal Year 2001-2020 (FY2001-FY2020) show annual donations/charitable payouts marginally exceeding (and in some cases fall short of) the federally mandated 5% minimum. In FY2020, for example, the Joseph and Rae Gann Charitable Foundation disbursed $2,258,100 in donations and expenses, 4.5% of the $49,816,184 fair market value of the Foundation's assets at the end of FY2019. Moreover, because the Joseph and Rae Gann Charitable Foundation's assets are invested in corporate stocks, assets within the Foundation have in recent years yielded annual gains close to the amount of money the foundation has disbursed in donations and expenses. In FY2019, for example, assets with the Joseph and Rae Gann Charitable Foundation produced revenues from interest and dividends, along with gains from asset sales, totaling $1,755,014, or 75% of the $2,331,932 that the Foundation granted in donations and expenses that year. 75% of the donations made by the Joseph and Rae Gann Charitable Foundation in FY2019 came from the interest gained from relatively untaxed securities, money acquired within the last business year, rather than from an actual direct donation by the family.

In FY 2020, the Joseph and Rae Gann Charitable Foundation disclosed capital gains (interest made by holding stocks) of $1,465,768 and paid the excise tax of 1.39% on these gains, for a tax bill total of $20,374. Had these gains been taxed as capital gains received by an individual or couple in the highest income tax bracket, the gains would instead have been taxed at 20% rate (leaving aside additional tax evasion tactics), for a total tax bill of $293,153. By holding securities in a private foundation, the Gann family was able to shield an additional $272,779.60 from taxes and maintain control of that wealth.

Still more important, private foundations can greatly reduce the estate tax paid by a family after the richest member dies and their assets (like cash, securities) are placed into the private charity holdings. In 2021, estate taxes were applied when an estate is worth over $11.7M (this will increase to $12.06M for the 2022 tax year). Circumventing this tax is obviously a goal of the ultra-wealthy. After leaving the exempted inheritance to their family (<$11.7M), rich people can circumvent the estate tax by leaving any non-exempted assets (>$11.7M) to their private foundation, a tax-exempt charity.

To return to the Joseph and Rae Gann Charitable Foundation, Rae Gann survived her husband by a year and died in 2004. In 2003, the Foundation disclosed $60,343,410 in assets and the estate tax exemption was significantly lower, meaning all estates of over $1M were subject to the tax. The tax rate for all assets over the exemption amount gradually increased to 40%, when the estate exceeded $1M more than the initial exemption sum. If the $60,343,410 in assets held by the Joseph and Rae Gann Charitable Foundation represented the entirety of Rae’s estate, and this had been left to her descendants outright, the tax bill for all inheritance in 2004 after that first $2M alone would have been $23,337,364 (not accounting for additional tax evasion tactics). Instead, the money remains in the foundation, which the Gann family continues to control today, and regularly makes “charitable donations” barely reaching the federal minimum requirements, withstanding capital gains losses (which are also tax-deductible).

From FY2001-FY2020, the Gann family used the Joseph and Rae Gann Charitable Foundation to funnel $9,571,412.67 into zionist organizations complicit in the occupation and genocide of Palestine. This does not include FY2015, FY2017, and FY2018, for which the Foundation did not itemize their donations. Almost $10M dollars were sent by one family in the united states to further the genocide of Palestine by funding propaganda, the occupation army, and normalization efforts. The Gann family exemplifies the rule, not the exception, when discussing private foundations and related financial vehicles.

Thinking about all the ways that the tax code protects wealth accumulation is exhausting, but important. Within a 15-year period, the tax code went from protecting $1M inheritances to protecting $12M inheritances. By strategically maintaining their assets in the present, the rich can wait for tax law even more favorable to them in the future. Rich families prefer private foundations to public charitable donations because public charities take their money and use it, while their private foundations can hold the money quasi-indefinitely, all while continuing to gather capital gains. As the rich further consolidate their political control, there will come a time when tax policy related to charitable donations will be even more favorable to them. Maintaining control over “donated” assets can only serve wealth consolidation.

Rather than benevolent ventures through which wealthy individuals give away their money for the public good, private foundations should be understood as strategic financial maneuvers through which the wealthy reduce the taxes they have to pay into public budgets, in exchange for committing to donate a portion of the (under-taxed) wealth held within their foundations to their preferred charitable causes. The Gann family uses the Joseph and Rae Gann Charitable Foundation as a tax-free stock portfolio for $38.5M of their familial wealth, while funneling derivative income from these stocks into organizations and institutions which support Israel's ethnic cleansing of Palestinians from their homeland.

Some examples of organizations supported through their private foundation include:

- $4,779,000 from fiscal years 2001-2020 sent to Gann Academy, named for their family following substantial donations. Gann Academy promotes israel through its curriculum and school clubs, glossing over the colonial nature of zionism.

- $223,100 from fiscal years 2001-2020 sent to Birthright Israel, which sends American Jewish youth on propaganda trips to Palestine, encouraging them to conflate Jewish identity with zionism and israel.

- $70,960 from fiscal years 2001-2020 sent to CAMERA, which stifles student speech on campuses, slandering anyone who supports Palestinians and describes israel as an apartheid regime.

- $3,866,095 from fiscal years 2001-2020 sent to Combined Jewish Philanthropies, a donor advised fund described below.

The donor-advised fund: a present and future threat

The most important rule regarding private foundations is the federal filing requirement of the 990-tax form. This form is a required annual filing for all 501c3 charities with substantial assets, and includes information such as total foundation assets, grants made in the past year and approved for future dispersal, the salaries of paid employees, and the make-up of contributions to the foundation, among other pieces of information. This filing allows some level of public insight into the financial influence of the wealthy on society. Rich people disdain this required transparency and have found a way to circumvent the public disclosure of charitable gifts while maintaining control over assets: the donor-advised fund.

A donor-advised fund (DAF) is a financial account established within a public charity or “sponsoring organization” for the purposes of making charitable donations. Like a private foundation, the funds donated must be used for charity and allow the donor to maintain control over where the funds are sent. Unlike a private foundation, there are no reporting requirements for DAFs, regardless of their size, and there is no payout requirement—annually or at any point, unless the sponsoring organization establishes one.

Because the DAF is run through a public charity, the larger entity performs all administrative duties as part of the account agreement and shields the donor from the public. When the rich donor sends money to a charity through their DAF, they can elect to have the public charity that holds their DAF credited with the donation. DAFs allow the wealthy to hide their monetary influence from the public, while the wealthy disclose to charities that they made a DAF gift, ensuring they receive praise, attention, and influence for their donations. To appease the donor with an eye towards future donations, public non-profits treat “anonymous” gifts with the utmost discretion. Further, donating to a DAF account is technically a donation to a public charity, and therefore increases the tax deduction available to the wealthy--50-60% of income for cash and 30% for long-term securities. By using a DAF, rich people can have the tax benefit of donating to a public charity, a unique level of privacy, and a similar level of control over assets that can be had with a private foundation.

Why would public charities sponsor these funds? As part of the administrative agreement, some DAFs have an expiration date, after which the public charity will take ownership of the assets. Throughout their lifetime, DAFs also allow for fee-taking by their parent charity. Some of the largest public charities facilitating national DAFs are actually “charities” attached to banks—such as Fidelity Charitable—meaning that ultimately the banks’ business model of ever-growing financialization is served by having even more money to launder. Money put in DAF accounts is usually invested in the stock market—the assets then continue to appreciate without accruing capital gains taxes, and the public charity’s financial management team extracts fees based on the performance of the financial account. Additionally, massive public charities will tack a management fee onto these accounts, syphoning funds that ostensibly are earmarked for charity. Fidelity Charitable reported that their DAF program accrued $15B dollars in capital gains from its establishment in 2011 through fiscal year 2020.

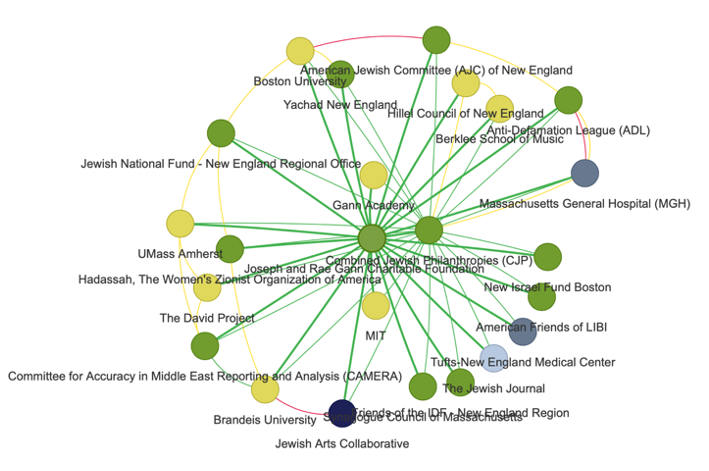

The Mapping Project contains an entry on Combined Jewish Philanthropies, a donor advised fund established in 1960 through a merger between two Jewish charities, Combined Jewish Appeal and Associated Jewish Philanthropies. In 2021, CJP was ranked as the largest non-profit in Boston. There are 60 recorded links between CJP and other Boston-area entities on the map, and the majority of them are financial.

Some ostentatious examples of funding provided to various organizations through CJP include:

- $1,793,864 sent to the JNF from fiscal years 2007-2020. The JNF is known for enabling the violent seizure of Palestinian land, planting trees on said land to prevent Palestinians from returning, and establishing fire departments to handle massive forest fires caused by said trees, which are not suitable for the climate of Palestine.

- $1,514,942 sent to The David Project from fiscal years 2007-2020, which exists to silence Palestinian and Palestinian solidarity activists on college campuses, as well as anyone who questions the zionist project. An additional $1,414,286 was sent to Committee for Accuracy in Middle East Reporting and Analysis (CAMERA), which has the same founder and goals as the David Project, during the same fiscal years.

- $20,303,700 sent to the Broad Institute from fiscal years 2007-2020, which contributes to ethnic cleansing (“gentrification”) in Boston, promotes the privatization of health care and publicly funded biomedical research, and also supports united states' imperial efforts. Unsurprisingly, CJP sent an additional $25,555,685 to MIT (affiliated with the Broad Institute) and $1,606,462 to MIT Hillel in the same period.

We can’t trace who initially donated this money to CJP in any meaningful way, which is scary. The amount of funds funneled through a DAF such as this can be massive, as demonstrated through the MIT and Broad Institute donation totals. When we do know the rich people behind some massive donations to CJP, it is because of their IRS mandated disclosures. From fiscal years 2001-2019, the Ruderman Family Foundation donated over $16 million dollars to CJP. But we can’t know where exactly this money flowed, because CJP acts to obfuscate the destination of the wealthy’s donations. We don’t know if Ruderman is giving money to MIT or to CAMERA—or just holding tight to the funds in the CJP-controlled DAF, waiting for a future time to donate.

DAFs are only increasing in popularity and are exacerbating the damage done by both private and public philanthropy.

All wealthy private citizens evade domestic wealth redistribution and many commit or support atrocities within the international community to further extrapolate resources and power (see other essays in this project for more information). The staggering amount of money funneled from private united states citizens to facilitate the occupation of Palestine should be a wake-up call, and a reminder that non-profits are complicit in the very worst crimes imaginable.